I Left My Wallet at Home and Paid for Everything Anyway — Here's What That Took

A walletless trip to Sheraton Mall exposed the gaps in Barbados' payments landscape. With BiMPay now targeting June 12, 2026, will instant interoperable payments finally close them?

One afternoon, I found myself at Sheraton Mall without my wallet or any way to tap and pay — just my phone and my banking apps, and a few items to pick up. What followed was an improvised lesson in the gaps that still exist in Barbados' payments landscape — and a preview of why the Central Bank of Barbados' upcoming instant payment system, BiMPay, has generated so much anticipation.

The Workaround

At two retailers in the mall, I asked whether they accepted direct deposits. One said yes in principle, but their process for verifying incoming transfers relied on logging into their bank's online platform — which happened to be down at the time. Without that confirmation, they weren't comfortable proceeding. A reasonable position, but a frustrating one.

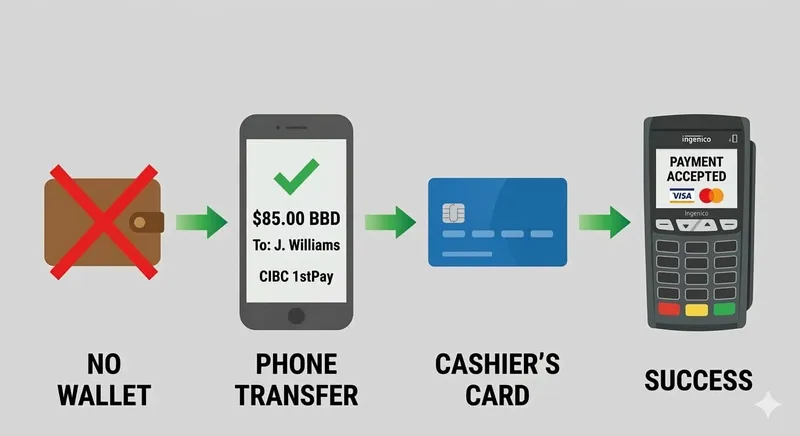

In both cases, the solution came from an unlikely place: the cashiers themselves. Both happened to be personal CIBC customers, which meant I could use CIBC's 1stPay — a person-to-person transfer service — to send funds directly to each cashier's personal account. They would then use their own debit card at the POS terminal to complete the transaction on my behalf, essentially processing it as though they were the customer.

It worked. But it was a workaround built entirely on coincidence — the right cashier, at the right bank, willing to improvise. 1stPay is a CIBC-to-CIBC service, so if either cashier had banked elsewhere, that option wouldn't have existed. And it's worth noting that 1stPay does deliver instant confirmation to the recipient via SMS, email, and app notification the moment a transfer lands — so the technology for real-time verification was there. The business banking platform being offline was a separate problem, at a separate layer, that no consumer-facing tool could fix.

That handled the essentials. For everything else, I took a different route entirely — leaving the mall, driving to a nearby Sagicor branch, and using their app to complete a cardless ATM withdrawal. Cash in hand, I returned to pick up the remaining non-essential items.

Multiple workarounds. Two trips. None of it should have been necessary.

The Underlying Problem

What the experience exposed isn't unique to that afternoon. It reflects a broader structural reality: even where digital payment tools exist in Barbados, businesses often aren't set up to use them flexibly. Verification processes get anchored to specific platforms. When those platforms go down, the fallback is either cash or improvisation.

Enter BiMPay

The Central Bank of Barbados has revised BiMPay's go-live date from March 31 to June 12, 2026, to allow completion of final interoperability testing across all participating institutions. It is Barbados' first national instant payment system, designed to settle transactions between individuals, businesses, and government in real time, around the clock, 365 days a year.

Critically, BiMPay is intended to be fully interoperable — it won't matter which bank the sender or receiver uses. Transactions are designed to complete in under 10 seconds, with both parties receiving instant confirmation. The system also supports digital wallets, meaning it doesn't require either party to hold a traditional bank account. All major commercial banks — CIBC Caribbean, First Citizens, RBC, Republic Bank, Sagicor, and Scotiabank — are confirmed participants, alongside several credit unions.

The Central Bank has confirmed that BiMPay will support merchant payments: according to their FAQs, users will be able to use it to buy groceries, fill up at the gas station, or even renew a driver's licence.

The Open Question

On paper, BiMPay addresses the friction points my experience exposed. Transfers would be instant and confirmed in real time across all participating institutions — no dependence on any single bank's platform being online. Interoperability removes the bank-matching problem entirely. And the 24/7 availability sidesteps the business-hours constraints that have long plagued ACH-based transfers.

But my experience suggests that infrastructure alone may not be enough. Even with 1stPay's instant notifications already in existence, that retailer's process wasn't built to act on them.

On the merchant experience, the Central Bank has since published details on how point-of-sale payments will work. BiMPay will support QR code payments — both static codes (where the merchant displays a code and the customer enters the amount) and dynamic codes (generated per transaction with the amount included). The system will also include Request to Pay, where a merchant sends you a payment request that you review and approve before any money moves. These are exactly the kind of purpose-built flows that could replace the workaround I described — no need for a cashier to swipe their personal card on your behalf.

The question is whether these flows will feel as effortless in practice as they sound on paper. That detail matters. The workflow matters as much as the technology.

The real question for BiMPay isn't whether the system can deliver instant, confirmed payments — it almost certainly can. The question is whether Barbados' merchants will be set up with intuitive, purpose-built flows that make accepting a BiMPay payment simpler than swiping a card, not more complicated.

That's a change management challenge as much as a technology one. And it's not something any payment rail, however well-designed, can solve on its own.

When BiMPay launches, whether it changes how a cashier at Sheraton Mall handles a walletless customer is a different question entirely — and one worth watching.

Questions about this topic?

Financial terms can be confusing. If you have questions about the article or ideas for what I should cover next, send me a DM.

Chat on Instagram